1.4 Setting the Context

Financial inclusion is embedded in the broader context of poverty-related issues impacting communities across Canada, Ontario and Waterloo Region. Individuals living in poverty are often limited in their access to appropriate, regulated financial products or services, including functioning bank and credit accounts, income tax support and financial advice (Fair, Gosse, Moore & Robson, 2008; Buckland, 2008). This exclusion also extends to circumstances where individuals are limited in opportunity, ability and confidence to make informed decisions about their financial situation (Fair et al.) Financial exclusion interacts with other forms of community exclusion, including exclusion from stable housing, employment and civic participation, creating cycles of instability and risk.

In Ontario today the right to social and economic security is in the spotlight. The recent Social Assistance Review (Lankin & Sheikh, 2012) and the Drummond report (Commission on the Reform of Ontario’s Public Services, 2012) reflect the competing factors that affect decisions about how and where our money should be spent. These reports highlight debates about how economic resources are divided between the competing need for social programs and deficit reduction. The Bank of Canada’s latest “personal debt crisis” (Maclean’s, March 2009) is another indicator of the pressures on personal and public expenditures, savings and balanced budgets. These pressures significantly affect people with low income as they struggle to meet their basic needs, provide for their families and children and manage the balance between debt, income and savings. Moreover, “the trend toward an increasingly credit-based economy married with the economic downturn starting in 2008 contributes to more individuals finding difficulty managing their finances.” (Marsh, Dildar & Janzen, 2010)

Financial services and financial literacy are increasingly important in the management of personal and household financial resources, such as employment income, public income benefits, retirement planning, and access to affordable credit (Social and Enterprise Development Innovations (SEDI), 2008). However, individuals living on low incomes face ongoing barriers to accessing and utilizing mainstream financial services. Financial services offered by banks and credit unions offer limited programs that meet the needs of people living on low incomes. Supports and services offered by governments and social service agencies are not always easy or straightforward to access.

When whole groups within our population are excluded from mainstream financial services, the issue becomes one of more than individual financial literacy. A shared, community-wide ownership of the problems and solutions is required. Banks, credit unions, governments, non-profits, and corporations all have roles to play in ensuring all community members have access to fair, high quality financial services that promote social and economic inclusion.

Financial Inclusion across Canada

It is widely recognized that greater financial inclusion requires multi-stakeholder involvement and commitment. Across Canada, there are a number of organizations, collaborations and initiatives working towards greater financial inclusion. The majority of these initiatives are in the domain of the non-profit and social sectors, with some government attention in the last few years primarily targeted at increasing the financial literacy of Canadians. While there is work to be done to coordinate efforts and resources as well as to promote stronger collaboration and more substantive change, there has been leadership at national, provincial and local levels.

Since 1986, Social and Enterprise Development Innovations (SEDI) has been working to expand economic opportunity for Canadians living in poverty. As a national nonprofit organization, SEDI promotes program and policy innovation, identifying and developing ideas that expand social and economic opportunity for all Canadians. Financial literacy is one of the primary program areas, the other two being saving and asset building, and entrepreneurship (www.sedi.org). SEDI has been an influential player at a national level, serving as advisor to the Government of Canada’s Task Force on Financial Literacy, and through funding from TD Bank Financial Group launching the Canadian Centre for Financial Literacy as well as the TD Financial Literacy Grant Fund.

As a division of SEDI, the Canadian Centre of Financial Literacy (CCFL) is dedicated to helping develop financial literacy among low-income Canadians (www.theccfl.ca). It offers a number of services and programs, including program development, training and an online community, designed for easy-to-use money management training for low-income groups through non-profit community organizations.

SEDI also manages the TD Financial Literacy Grant Fund. First of its kind in Canada, this Fund provides grants to charitable or other non-profit organizations that serve low income and otherwise economically disadvantaged persons and groups in Canada (http://www.sedi.org/grantfund). The Fund prioritizes projects that support innovation, research and development, and strategic program development for people living in Canada who may normally be excluded from mainstream financial organizations, enabling them to develop skills, knowledge and confidence in financial issues.

In 2001, the Financial Consumer Agency of Canada (FCAC) was established under the Financial Consumer Agency of Canada Act to consolidate and strengthen oversight of consumer protection measures in the federally regulated financial sector, and to expand consumer education (http://www.fcac-acfc.gc.ca). As a federal regulatory agency, FCAC is works to protect and inform consumers of financial products and services. Its responsibilities include informing consumers about their rights and responsibilities when dealing with financial entities as well as providing information and tools to help consumers understand, and shop for, financial products and services.

In 2009 the Government of Canada appointed the Task Force on Financial Literacy. Comprised of 13 members drawn from the business education, community organizations and academia, the Task Force’s mandate was to provide advice and recommendations to the Minister of Finance on a national strategy to strengthen the financial literacy of Canadians. A report was made public late 2010 underscoring the need for a national strategy and strong leadership as well as the shared responsibility of stakeholders. In 2010, the Toronto G20 Summit put forward a set of principles to support greater financial inclusion, which were intended to be used to inform a plan of action for improving access to financial services.

There are numerous government and non-profit initiatives across Canada that are aimed at supporting financial literacy. For example, the FCAC offers free financial literacy program resources aimed at high school-aged youth and young adults. The Ontario Ministry of Education has also introduced curriculum changes to include financial literacy for student's from grade 4 to 12, beginning in September 2011 (http://www.edu.gov.on.ca/eng/surveyLiteracy.html)

Another initiative designed to support greater financial literacy is the Investor Education Fund (IEF, http://www.getsmarteraboutmoney.ca). Established as a non-profit organization by the Ontario Securities Commission, the IEF develops and promotes unbiased, independent financial information, programs and tools to help consumers make better financial and investing decisions. In addition to offering online resources available for all Canadians, IEF seeks partnerships with non-profit community-based organizations and institutions to develop financial literacy programs for those with an identifiable need for learning how to manage finances and investment.

The two national credit counselling organizations in Canada are Credit Counselling Canada (CCC) www.creditcounsellingcanada.ca and Canadian Association of Credit Counselling Services (CACCS) www.caccs.ca. Their member organizations offer free counselling services to Canadians in need of support to manage credit and debt. Ontario also has its own association, as do many of the provinces. The Ontario Association of Credit Counselling Services (OACCS) www.oaccs.ca aims to improve the financial literacy and well-being of Canadians and provides an accreditation program in non-profit credit counselling for its member agencies. An accredited credit counselling agency must adhere to standards of practice, expertise and ethics.

As these initiatives show, there are resources available to Canadians seeking to gain greater financial literacy. What distinguishes programs supporting financial inclusion, however, is a focus on meeting the needs of Canadians living with low income. Through research, advocacy, and policy review, SEDI has played a strong leadership role in supporting greater financial inclusion among the most vulnerable. Leadership is also found at the community level where innovation and support are emerging across the country.

Community-based initiatives have been instrumental in meeting the needs of individuals not being served by traditional banks. These efforts are usually small scale grassroots initiatives, and have ranged from community banking projects to individual financial counselling. The research report In Search of a Local Alternative (Marsh, Dildar, Janzen, 2010) reviews a number of Canadian examples of community-based initiatives seeking to support greater financial inclusion, such as those found in:

- Winnipeg, Manitoba, a unique community banking project is offered by a partnership between the Assiniboine Credit Union and a non-profit organization called the North End Community Renewal Corporation (NECRC). Services include an ID clinic, one‐on‐one financial counselling, and access to low-cost micro‐loans.

- Toronto, Ontario, St. Christopher House and the Jane/Finch Community and Family Centre both offer Financial Advocacy and Problem Solving (FAPS) to low income people in Toronto. They provide one-on-one individualized service, as well as workshops.

- Quebec, the Caisse Populaires Desjardins and several consumer advocacy groups partner to offer small, short-term loans for approximately $500 and budget management advisory services (Desjardins, 2010).

Some organizations have outreached and developed partnerships with other agencies, local governments, and financial institutions to share resources and referrals, to align their efforts, and collaborate on joint actions. Examples of community-wide initiatives in Canada are found in:

- Edmonton, Alberta, the Alberta Asset Building Collaborative is a 40-member group of not-for-profits, businesses and government committed to financial literacy and asset development. One of their regular activities is to host Financial Information Fairs for low income individuals

- North York, Ontario, the Black Creek Financial Action Network (BCFAN) started meeting monthly in late 2011 to bring together service providers working in the Black Creek area, along with academics and students from the York University - TD Community Engagement Centre.

Financial Inclusion in Waterloo Region

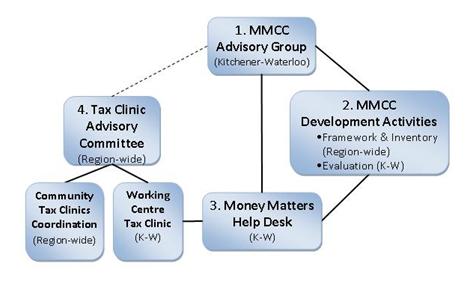

Locally, there is strong commitment at the Regional and community level to work collaboratively in pursuit of a more inclusive and welcoming community. In Kitchener-Waterloo for example, the Money Matters Community Collaborative (MMCC) is comprised of a range of stakeholders, including community-based agencies, regional government, community members and local financial institutions. The Money Matters Collaborative was launched in 2010 as an outcome of a research project led by the Centre for Community Based Research on the local use and impacts of pay-day lending. After extensive community consultation, the collaborative was formed with the specific purpose of increasing financial inclusion for economically disadvantaged individuals in Kitchener-Waterloo and the broader regional community. It includes the following four components as described and diagramed below:

1) Money Matters Community Collaborative (MMCC) Advisory Group – has been meeting 6-10x/year since 2010 and includes approximately 30 community partners including financial institutions.

2) Money Matters Community Collaborative (MMCC) Development Activities – defining a framework for financial inclusion, documenting an inventory of relevant supports and services, and completing evaluation activities.

3) Money Matters Help Desk – 1 FTE provides 30 hrs./week direct individual financial literacy education and support (12 hrs. drop-in clinic and 18 hrs. appointment and follow-up) and up to 5 hrs./week to MMCC activities (Advisory Group, Developmental Activities, etc.)

4) Tax Clinic Advisory Committee – currently has an informal connection to the MMCC – activities include direct delivery of a tax clinic (appointment, drop-in and drop-off) as well as the coordination of other currently existing community tax clinics for people living with low income.

Figure 1. Money Matters Community Collaborative Structure

The role of The Working Centre in MMCC includes providing “backbone” support to the MMCC Advisory Group, Developmental Activities, and Tax Clinic Advisory Committee. They directly deliver the Financial Literacy Outreach Project and Tax Clinic.

The Working Centre has included a “Living with Less Money” section on their website which may also house this inventory document as well as other information about the Money Matters Community Collaborative (http://www.theworkingcentre.org/less/index.html).

In addition to the Money Matters collaborative, there are a number of efforts to support greater financial inclusion among agencies and services in the region. These programs and services are designed to meet the needs of those living with little or no income to manage their finances and maintain a high level of community inclusion. Programs available through banks, credit unions and community agencies focused specifically on financial management are detailed in this inventory.